When you’re looking for a therapists, one of the first questions many people ask themselves and the therapists they call is “Do you take my insurance for therapy”?

We get this questions everyday on the phone and most people who want to use their insurance end up giving us a call back after a couple of weeks because they had so much trouble finding an in-network therapist. In this article I want to talk about the pros & cons of using insurance for therapy.

In the end, choosing an out of network therapists gives you complete control over your therapy – there are no waitlists with an out of network therapists, you can choose exactly who you see and find an expert for your needs, you don’t have to meet a crazy high deductible and there are no surprise bills or co-pays.

The good news is you have choices and that is our job, to help give you as much information as possible to make an informed decision.

*Note: the therapy and counseling we provide is of a significantly higher quality and ultimately the same price than what you will find at online therapists like Betterhelp.

A primer on how insurance works.

I know how frustrating and confusing the entire insurance system is. So let me break down how insurance works, because no one ever tells you this stuff!

When it comes to therapy (an all medical treatments) you have 2 options:

1) In-network therapy

2) Out of Network therapy.

First your specific insurance policy must have coverage for Mental Health Services. Insurance companies are not required to offer this as an option, so you would need to verify that you even have coverage.

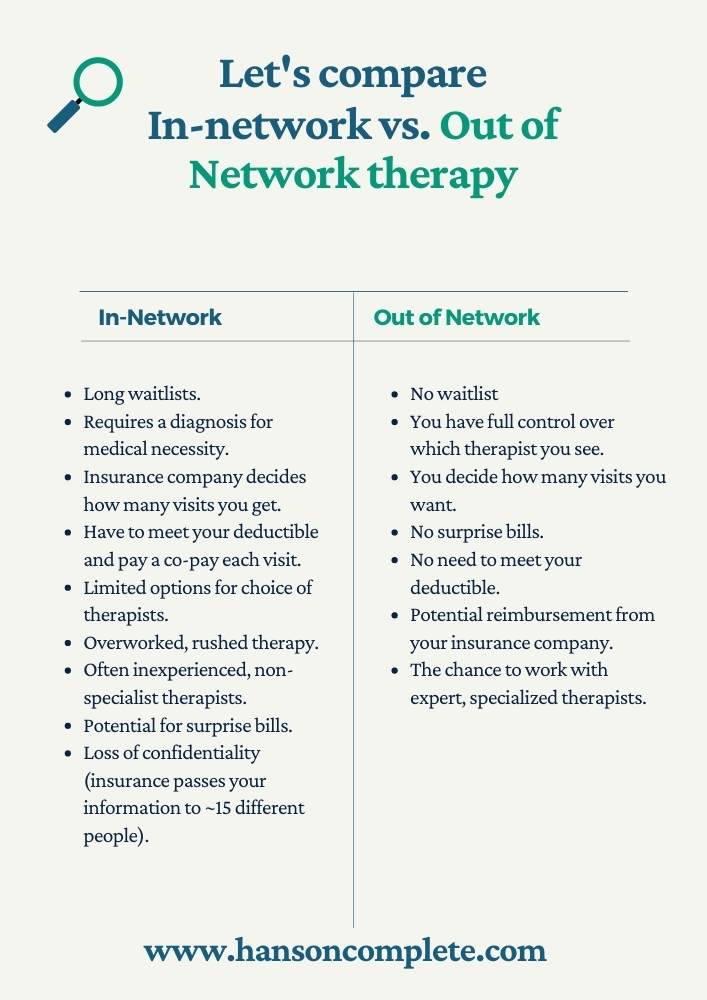

An In-Network Therapist has signed a contract with your specific insurance company and all care will be dictated by that contract. This requires a diagnosis to prove medical necessity of your care. This contract also dictates who you can see and how many visits you can have with them. Since mental health care isn’t considered “essential” by insurance companies, you have to meet your deductible.

So what is a deductible?

Deductibles: This is a set amount of money that you must pay before the insurance company starts to pay for certain services. The average deductible is between $4,000 and $8,000 per year.

When you have a high deductible, your health insurance premium (your monthly bill for health insurance) is often smaller. Some people choose a high deductible if they think they will not need a lot of medical care, because then their monthly payments are lower.

Once you reach your deductible for the year, then your insurance company may pay for a larger part of your health care costs. At each visit you would then be required to pay a co-pay which is on average of $25-$50 per therapy session.

What are the downsides of seeking out an In-Network Therapist or Counselor?

First you have to find a therapist in your network. This can include very long waitlists to be seen and some people have to wait weeks or even months to see an in-network therapist.

Secondly, Since insurance companies make it very difficult to get reimbursed for the treatments provided, you usually only find therapists in-network who have significantly less experience, are less specialized and who are generally very overworked and burned out.

Third, to get your therapy sessions covered, your therapist or counselor will have to provide your insurance company with a diagnosis to support a medical necessity for care. Since most of the problems people come to therapy are not so severe they don’t allow you to live your everyday life, justifying a medical necessity diagnosis can be tricky.

Fourth, there is a loss of confidentiality that can occur when you use your insurance for therapy. Once your notes leave your therapists office, they can pass between 15+ people in the insurance companies office.

So Let’s Re-cap the Downsides of In-Network Therapy

- Long waitlists.

- Treatments are controlled by insurance company – including the # of visits and who you can see.

- Less experienced, burned out therapists.

- Requires meeting a deductible that could be very high.

- Requires a diagnosis.

- Potential loss of confidentiality when your notes leave the office.

A Better Option, Out of Network Therapy

The good news is you have choices and that is our job, to help give you as much information as possible to make an informed decision.

Since finding an in-network therapist has so many issues the best option we’ve found after working with thousands of clients over the last 10 years is Out of Network Therapy.

This means you get to choose whoever you want to go to and you pay a simple flat fee for each session. No insurance company can tell you how many visits you get. You don’t have to be on a long waitlist. You can choose a specialist. The counselors you choose will have more experience and won’t be burnt out. You don’t have to meet a large deductible. There are no surprise bills.

All in all, working with an out of network therapist is just a simpler process that doesn’t require the hassle that comes with insurance.

The good news is that your out of network therapist can provide you a superbill (a special bill with all the required codes) that you can send to your insurance company and they will potentially reimburse you for your visits.

So working with an out of network therapist will provide you with a better therapy experience.

The Next Step

Click the button below to setup a short phone consultation to see if we’re a great fit for you!